MyDebit Overview

Introduction

MyDebit Scheme is a payment application that enables Cardholders to use their ATM card to pay directly from their bank account via a POS terminal and a dual-interface which supports both contact and contactless transaction.

The parties involved in the MyDebit scheme are:

- PayNet: Provides the central switching, clearing and settlement functions for all MyDebit transactions.

- Issuer: Validates the authorisation on the debit request to MyDebit System as well as processing the debit request to Cardholders account.

- Acquirer Bank: Financial Institution authorised by PayNet or Bank Negara Malaysia to recruit merchants and to deploy MyDebit terminals to support MyDebit Scheme.

- TPA: A Non-Financial Institution authorised by PayNet or Bank Negara Malaysia to recruit merchants and to deploy MyDebit terminals to support MyDebit Scheme.

- Merchant: A business, Government Agency, or organization that offers goods and/or services and accepts MyDebit as one of the mode of payments at the counter.

- Cardholder: A person who holds MyDebit card issued by an Issuer that maintains the accounts (i.e. Savings / Current) that could be accessed by such card.

info

Check out the glossary which provides definitions and explanations of frequently used terms for MyDebit Secure. You may also refer to Abbreviations which been used in this document.

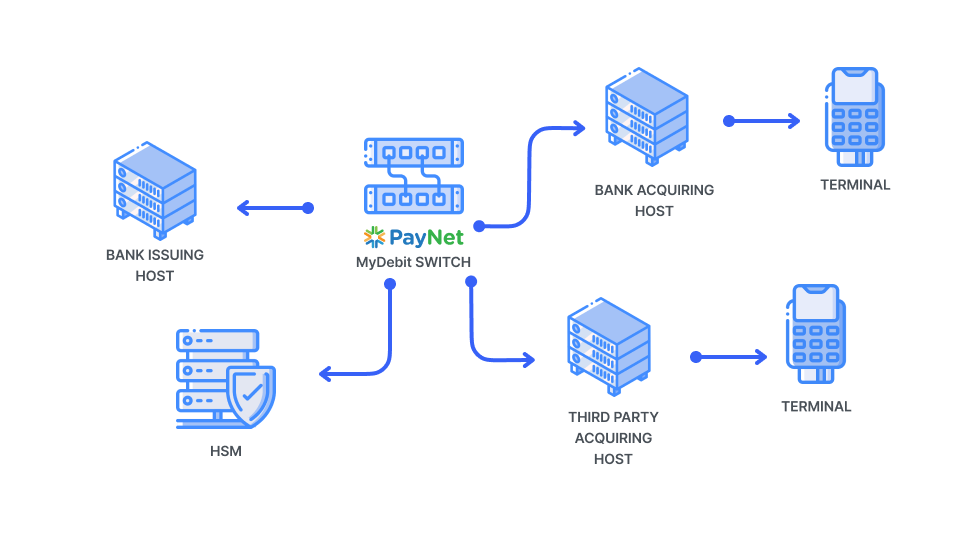

MyDebit System Overview between PayNet and Participants

- Participants’ hosts shall connect to the MyDebit System using the TCP/IP protocol with effect from 1 January 2017.

- The Terminals are connected to the Participant’s processor which will route all transactions to MyDebit System. These transactions are then sent to the Issuer’s processor for authorisation process.

- The Issuer will acknowledge the transaction by sending a response to MyDebit System with an approval or decline response code.

- The MyDebit System will then forward the transaction to the Acquirer with the same response code. The Acquirer will then deliver the response to the Terminals to complete the transaction.

MyDebit System Connection

- Connection to MyDebit System is limited to the Participants of the MyDebit Scheme only.

MyDebit Connection Guideline

- PayNet may modify or waive the requirements of this section with prior notification to Participants.

- Any Participant which seeks a waiver on the requirements of this section shall submit a petition to PayNet before such entity becomes a Participant, explaining the reasons why such waiver should be granted.

- Where an Acquirer agrees to accept other Participants’ cards, the Acquirer must make changes to their MyDebit message format and route the transactions to PayNet for authorisation including PIN encryptions.

- The Issuer will have to develop the necessary software to receive transactions from PayNet, to translate PINs, verify PINs, and authorise transactions.

- Participants may use the existing network connection that support ATM transaction for MyDebit transaction.

Type of Transactions

The MyDebit System shall only support real-time online transactions. Offline transactions as well as Stand-in mode processing is not supported by MyDebit System. The supported transactions are:

Purchase

- A financial transaction consisting of payment information of goods or services purchased/rendered initiated by the Cardholders. The transaction is captured and submitted to the Issuer for payment authorisation.

- Process Flow for Purchase:

- The transaction message flow below explains the summarised overview of the message transfer between the Acquirer, MyDebit System and the Issuer for a Normal Purchase.

| Steps | Description |

|---|---|

| 1 | The Acquirer sends a 0200 external message to MyDebit System. |

| 2 | MyDebit System then sends the 0200 external message to the Issuer for authorisation. |

| 3 | Issuer authorises the transaction and sends a 0210 response external message to MyDebit System |

| 4 | MyDebit System then sends the 0210-response external message to the Acquirer to be completed. |

Purchase Cancellation

- A Purchase Cancellation is a financial transaction initiated by a Merchant or an Acquirer to cancel an approved purchase transaction and process a refund to the Cardholder. The transaction must be submitted by the Merchant or service provider within the same day of the purchase transaction intended to be cancelled. However, the retrieval of the approved purchase transaction data will depend on the capability of the following:

- Whether the Acquirer can store and retrieve purchase transaction data from their host; or

- Whether the original purchase transaction data had been uploaded to the host; or

- Whether it is uploaded and secured in the MyDebit System database.

- Process Flow for Purchase Cancellation:

- Whether the Acquirer can store and retrieve purchase transaction data from their host; or

- Whether the original purchase transaction data had been uploaded to the host; or

- Whether it is uploaded and secured in the MyDebit System database.

| Steps | Description |

|---|---|

| 1 | The Acquirer sends a 0200 external message to MyDebit System. |

| 2 | MyDebit System then sends a 0200 purchase cancellation message to the Issuer. |

| 3 | Issuer acknowledges the transaction and sends a 0210 purchase cancellation response message to MyDebit System. |

| 4 | MyDebit System then sends the 0210 purchase cancellation response message to the Acquirer. |

Purchase with Cash Out

- A financial transaction consisting of payment of goods or services, and cash withdrawals in the same transaction.

- For Purchase with Cash Out, the transaction amount is divided into two categories, the purchase amount and the Cash Out amount. The purchase activity remains the same as the normal Purchase transaction. Please refer to Process Flow for Purchase as mentioned earlier.

- Authorisation Request (0200) will be sent to the Issuer host via PayNet MyDebit switch. The message will contain additional fields that will carry purchase via MyDebit and Cash Out amount withdrawn. The Issuer bank verifies the request and deducts Cardholder’s account for MyDebit, Cash Out withdrawal and replies with the Authorisation Response (0210) message.

- For Purchase with Cash Out, the Cash Out amount must not be more than RM500 per transaction.

- Process Flow for Purchase with Cash Out:

- The transaction message flow below explains the summarized overview of the message transfer between the Acquirer, MyDebit System and the Issuer for a Purchase with Cash Out.

Steps Description 1 The acquirer sends a 0200 external message to MyDebit System. 2 MyDebit System then sends an external message to the Issuer for Cash Out authorisation. 3 The Issuer then authorizes the Cash Out and sends a 0210 response external message to MyDebit System. 4 MyDebit System then sends the 0210 response external message to the Acquirer to complete the Cash Out transaction. - Acquirers shall at a minimum adopt the following transaction flow for MyDebit Cash Out at the terminals:

- Enter purchase amount

- Insert MyDebit card

- Enter Cash Out amount

- Enter PIN

- Acquirers shall at the minimum display purchase amount and Cash Out amount separately on the receipts

- Acquirers shall ensure that the amount that is keyed in as ‘zero’ for MyDebit Cash Out is to be treated as a purchase transaction.

- Participants shall display the MyDebit Cash Out amount separately from the purchase amount in the Cardholder’s account statement.

- The transaction message flow below explains the summarized overview of the message transfer between the Acquirer, MyDebit System and the Issuer for a Purchase with Cash Out.

Purchase with Cash Out Cancellation

- The purchase activity remains the same as the normal Purchase transaction. Refer to Process Flow for Purchase as mentioned earlier.

- Cashier will initiate the void function on the terminal and key in the invoice number.

- Process Flow for Purchase with Cash Out:

- Cardholders will need to slot their ATM card, enter the PIN and select account type at the terminal.

- The acquirer will send a 0200 purchase cancellation message to the Issuer host via PayNet MyDebit switch.

- The Issuer bank acknowledge by sending a 0210 purchase cancellation response.

- The transaction message flow below explains the summarised overview of the message transfer between the Acquirer, MyDebit System and the Issuer for a Purchase with Cash Out Cancellation.

| Steps | Description |

|---|---|

| 1 | The Acquirer sends a 0200 external message to MyDebit System. |

| 2 | MyDebit System then sends 0200 cancellations external message to the Issuer. |

| 3 | Issuer acknowledges the transaction and sends a 0210 Cash Out cancellation response message to MyDebit System. |

| 4 | MyDebit System then sends a 0210 cancellation response message to the Acquirer. |

Pre-Authorisation

- A pre-authorisation entails earmarking an amount of funds in a Cardholder’s bank account pending completion of a MyDebit transaction where the actual transaction amount cannot be determined at point of purchase initiation. The earmarked funds cannot be used and the earmark will only be removed after the transaction is completed.

- A pre-authorisation is typically used to facilitate transactions using OPT at self-service petrol pumps.

- Process Flow for Pre-Authorisation:

- For pre-authorisation involving transactions at OPT, the Issuer has to release the earmarked funds and debit the actual transaction amount after the sales-completion message is received from the Acquirer

- In the event the Issuer does not receive the sale-completion message from the Acquirer, the Issuer shall hold the earmarked funds in accordance to the revised Debit Card and Debit Card-i policy document issued by BNM on 2 December 2016.

- For pre-authorisation arising from transactions at OPT, the pre-set or configurable amount shall be at a minimum of RM0.01

- An Acquirer shall ensure that the pre-set amount menu or button at OPT is enabled and ensure clear instructions is given to the Cardholder to enter the required pre-authorisation amount.

- An Acquirer shall ensure that the final sales-completion is immediately send to Issuer as soon as the fuel nozzle is placed back on the pump. In exceptional cases, if the Issuer did not receive the sales-completion amount immediately, Issuer shall earmark the funds for no more than three (3) Calendar Days (T+2). Any discrepancies which arises from the Acquirer’s delay in responding will be treated as a dispute and will be handled via the MyDebit ECMS. The Acquirer shall be responsible to pay for the disputed amount

- An Acquirer shall ensure that the sales-completion released to the Issuer shall not exceed the pre-authorisation amount selected by the Cardholder. Otherwise, the Acquirer will be responsible to pay for the disputed amount

- The Pre-Authorisation service is as set out in the Overlay Service Procedures for MyDebit Pre-Authorisation Service effective on 1st April 2021.

- Participants are required to support MyDebit Pre-Authorisation at Other Segments as an Issuer no later than 1 April 2022 by fulfilling the requirements for MyDebit Pre-Authorisation acceptance at other market segments.

Card-Not-Present (CNP)

- The Card-Not-Present is a service that enables cardholders to perform an online payment transaction when the cardholder is not physically present at the merchant.

- The Card-Not-Present service is as set out in the Overlay Service Procedures for MyDebit Secure (Card-Not-Present) service.

PayNet Tokenisation

- PayNet Tokenisation is a service that enables a central standardised process of replacing the 16-digit MyDebit card number with an encrypted Token that can only be used at the identified online Merchant. This Token can then be stored at the Merchant for a more frictionless customer experience without the normal risks of storing the card number as utility of the Token is restricted.

- The PayNet Tokenisation service is as set out in the Overlay Service Procedures for PayNet Tokenisation service.

Payments

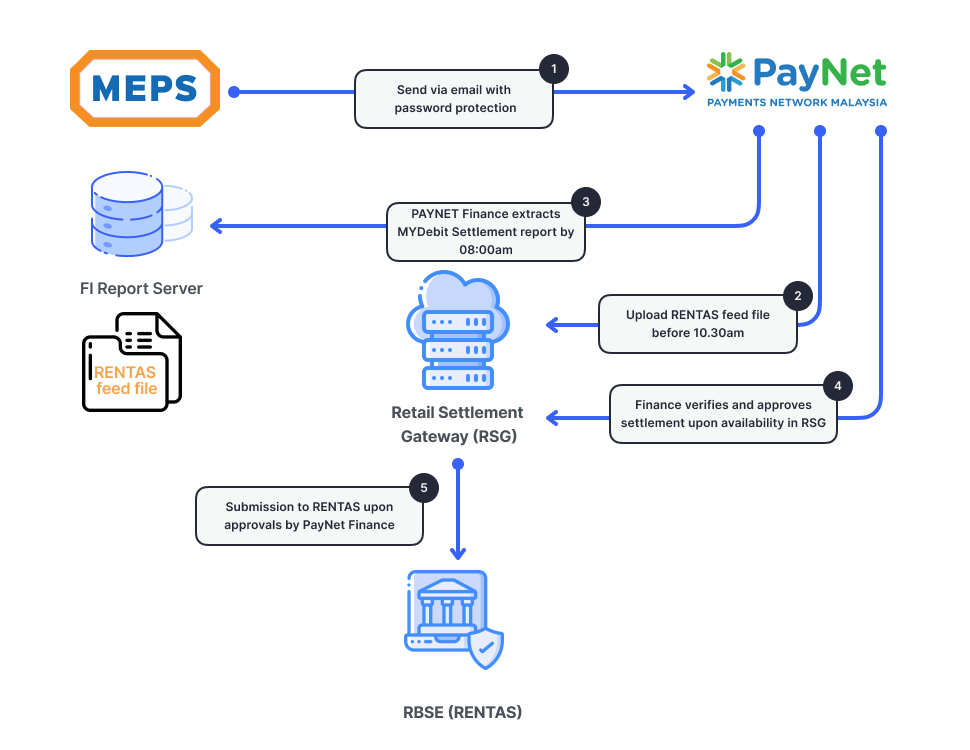

- The following diagram depicts MyDebit settlement via RSG process flow:

- Debit from Participants shall be made via RENTAS to PayNet’s Settlement Account no later than 11:30 am. PayNet will also credit the Participants via RENTAS from its Settlement Account no later than 11:30 am.

- If there should be any event where PayNet is unable to get the full settlement payment from Participant, the Participant is subjected to penalty interest.

- The settlement payment shall be made as follows: -

| Transaction Processed On | Description |

|---|---|

| Monday - Friday | Next business day |

| Saturday - Sunday | Monday |

| Holiday | Next business day |

Note: PayNet will observe the National Holidays and holidays of Kuala Lumpur Federal Territory.

- All Participants will settle with PayNet based on PayNet net settlement totals (*). For transactions processed on Saturday and Sunday and on holiday as observed by PayNet, each Participant shall settle with PayNet the net settlement total on the next business day.

- *Net settlement totals for MyDebit will be sent through the Daily MyDebit Settlement Report.7. ddd

- Upon settlement of a dispute lodged via the ECMS, Acquirers are required to remit the disputed amount to MyDebit Settlement Account by T+1.

- Failure to settle by T+1 will result in penalty of RM300 per day for late settlement. (Only applicable to TPA)

Reports

- The following reports will be produced daily for each Participant:

| No | Transaction Processed On | Description |

|---|---|---|

| 1 | Daily MyDebit Settlement Report (SETL01) | via FTP |

| 2 | Daily Detail MyDebit Transaction Report (STAT09) | via FTP |

| 3 | Daily Reconciliation File (Recon/Journal) | via FTP |

| 4 | ECMS Dispute Settlement Report | via FTP |

- The Daily MyDebit Settlement Report and Daily Detail MyDebit Transaction Report will be made available to each Participant by 6.00a.m on the next working day after each daily cycle. Reports will be compressed before being made available via transfer mode, via Secured Files Transfer Protocol (sFTP) to Participant.

- In the event the reports cannot be delivered via the sFTP, PayNet will send the report via email.

- PayNet shall assume Participants’ have received the reports if there is no feedback from the Participant by 11:00am.

- PayNet will retain the above reports for a period of seven (7) years from the date of the reports or such other period as required under statute and thereafter destroy them.

- The reports produced would be at the discretion of each Participant. However, it is recommended that the daily transaction journals be produced to aid with tracing and reconciliation with the Settlement Summary Report.

- Each Participant must maintain logs of every financial transaction processed in PayNet network.

- Transactions must be extracted from the log daily at cut-over time, based on the capture-date within each transaction, for the accumulation of Acquirer and Issuer settlement total.

- In the event other medium is used, the reports from PayNet will be made available by 9:00am on the next working day after each daily cycle. Therefore, Participants should provide an official identification of the person who will collect the report.

- The person appointed will be required to write his/her details in the PayNet report collection book. The person may also be required to show his / her Malaysian identity card for verification.

- It is the Participants’ responsibility to have their own records for the report collection.